The UK government, along with many governments around the world, is actively exploring the implementation of Central Bank Digital Currencies (CBDCs) as the next evolution of money.

This blog will unpack what CBDCs are, and why a growing number of people, from financial analysts to business leaders and even policymakers, are sounding the alarm, with many describing them as “Orwellian”, pointing to the level of government monitoring and control they could introduce.

Let’s dive in.

What are Central Bank Digital Currencies?

Put simply, a Central Bank Digital Currency is a digital version of a country’s official currency, issued directly by its central bank.

In the UK, this would effectively be a “digital pound”, issued by the Bank of England.

But isn’t money already digital?

Good question, and the answer is yes. Most of the pounds in circulation today are already digital. The key differences with CBDCs are who issues them and how much control they have.

Currently, the digital money we use today is managed within a network of commercial banks. This means there is a degree of decentralisation and also a separation between individuals and the government.

If the UK implements CBDCs, it would change the system to a centralised one where the Bank of England has complete visibility and control over all your transactions.

Moreover, this is coming at a time when the world’s financial infrastructure and technology is being updated, and the introduction of “programmable money” is drawing nearer.

What is “Programmable Money”?

Programmable money is digital money with rules and conditions embedded that grant the issuer new powers and control over your money and how you spend it.

Here are some potential features of programmable money:

- Expiration dates where money must be spent within a certain period or it becomes invalid

- Restrictions on what can be purchased, limiting spending to approved categories

- Controls on when and where money can be used, based on time or location

- Automated tax payments at the point of transaction

- Freezing your funds as punishment for speech or behaviour the government doesn’t like

A shift to programmable money paves the way for increased control for the issuer. For this reason, a growing number of people are voicing concerns over granting the government that level of power over your money through CBDCs.

The role of digital IDs

In 2025, the government announced plans for a national digital ID scheme in the UK. While their reasoning at the time was that it would help to crack down on people working illegally, the reality is digital IDs are an essential component for CBDCs and programmable money to work.

If implemented, digital IDs would give the government the ability to verify your identity across digital platforms, enabling:

- Digital connection between your identity and financial activity

- Visibility over your transactions

- The ability to apply rules and restrictions on your money

The combination of digital IDs with CBDCs opens the door to an unprecedented level of government control over your money.

Why owning gold is more important now than ever

If you hold the majority of your savings in pounds, not only is inflation silently eating away at your purchasing power, but increasingly the government is trying to grant itself more visibility and control over your finances.

Gold is a globally recognised asset that has been used as a store of value for thousands of years. It has a limited supply and is not tied to the policies of any single government.

In a context where the government controls how you spend your pounds, gold offers you an alternative. It is accepted and traded across the world, and can’t be monitored or controlled by any single government in the same way fiat currencies can.

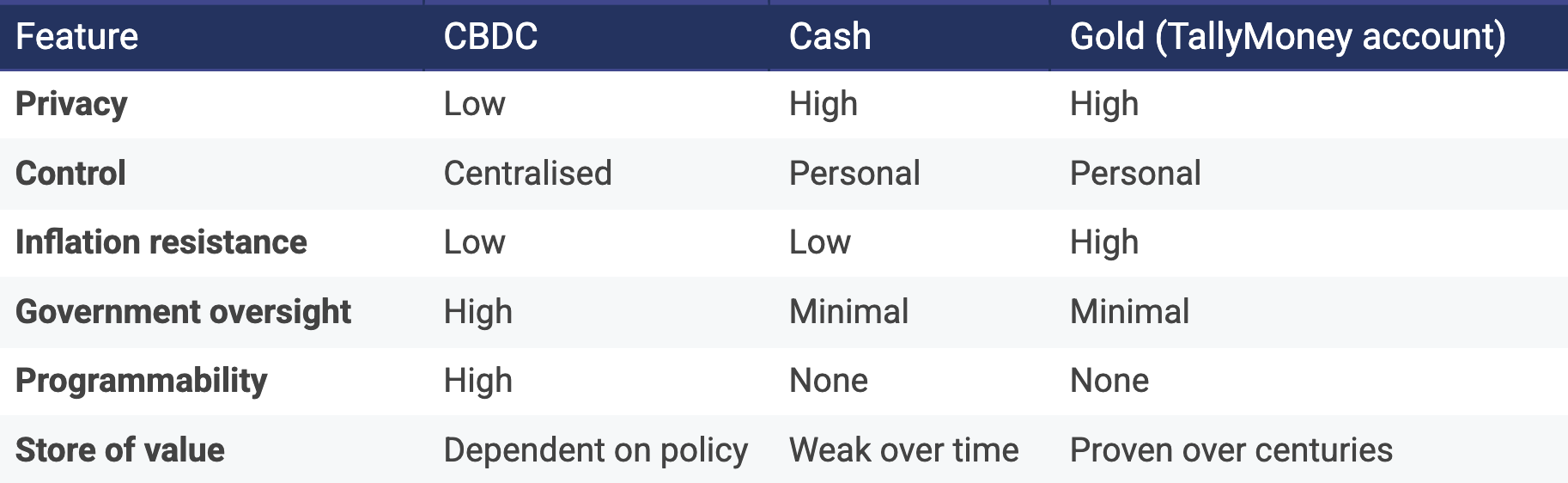

CBDCs vs Cash vs Gold

A modern approach with TallyMoney

Historically, owning physical gold has come with some drawbacks. Firstly, there is the responsibility of storing and insuring your gold yourself. Secondly, physical gold can’t really be used to buy things.

But in the age of technology, gold is getting a digital makeover, and TallyMoney is leading the way.

A TallyMoney Account lets you convert your pounds into gold instantly, and spend from your balance whenever you want in any currency. You get a Tally Debit Mastercard® which you can use anywhere in the world. For all practical purposes, a Tally Account works just like a regular bank account.

Crucially however your Tally Account can’t be monitored or controlled by the government the same way your pounds (in the form of CBDCs) could.

In an age where government control and surveillance is increasing, the pounds in your bank are shifting from neutral units of value to a digital tool of control. TallyMoney gives you an alternative to this Orwellian future.